Client Login

Client Login

Fed Chairman Powell Hawkish Talk: Fed Policy Remains Loose

Investing Environment Review and Outlook – Volume 55

Despite the recent equity volatility and negative headlines, conditions remain bullish for equities. The strong economy, loose Fed and Q4 combination we outlined in October remains in effect today. Aside from higher inflation reports, since the November letter there were three significant developments. First, one of the best coincident economic indicators, the ISM manufacturing index, improved to 61.1 in November, reaching the 99th percentile of readings since 1990 and confirming economic strength is not an issue. Second, some dramatic headlines combined with the brief 4.1% December S&P 500 decline resulted in a dampening of the extreme investor positioning seen at the November 18th peak. Finally, on November 30th Fed Chair Powell testified, among other things, that inflation is no longer transitory, marking a potential inflection point for Fed policy. This month we discuss Fed Policy, inflation and the shift in investor positioning. U.S., foreign- developed, and emerging markets equities remain a bullish 5 rating along with gold. Long-term bonds remain a cautious 2 rating and commodities remain a neutral 3.

Fed Chairman Powell Hawkish Talk: Fed Policy Remains Loose

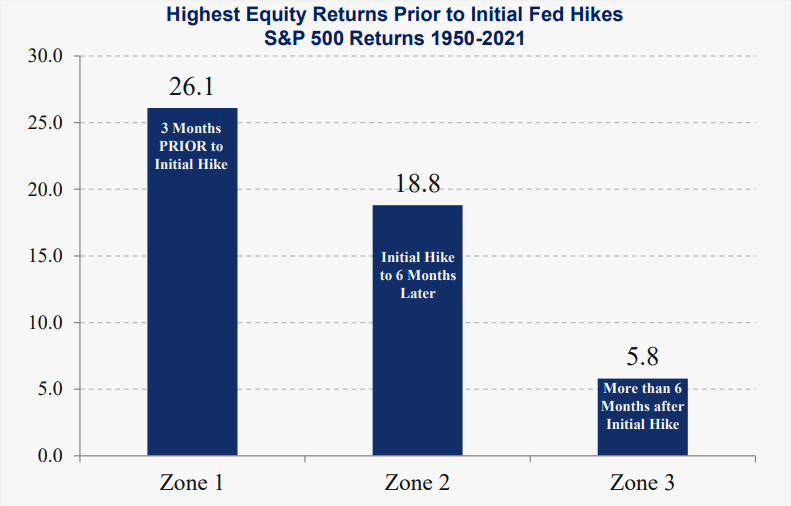

On November 30th Fed Chairman Powell finally rescinded the use of the word transitory, with a decidedly more hawkish tone than we have heard all year. Aside from the dubious timing, just 8 days after Powell was renominated, it means the taper will likely go faster than expected, and the assumption is interest rate hikes will begin sometime in 2022. It begs the question, does the rhetoric mark a shift in Fed Policy and what does it mean for equities? To find out, we broke historical Fed policy into zones. The first was 3 months prior to the initial interest rate hike. The second was from the initial hike to 6 months later. And the third was more than 6 months from the initial hike to the first interest rate cut. The results were telling. In the first zone 3 months prior to the initial hike, the S&P 500 returned the most at 26.1% annualized and a 94% probability higher. In the second zone, after the initial hike for the first 6 months, the S&P 500 returned 18.8%. In the last zone, more than 6 months after the initial hike, the S&P 500 returned just 5.8%. In other words, intent is not bearish for equities, and actions speak louder than words.

Inflation 6.8% Y/Y in November: Positive for Equities

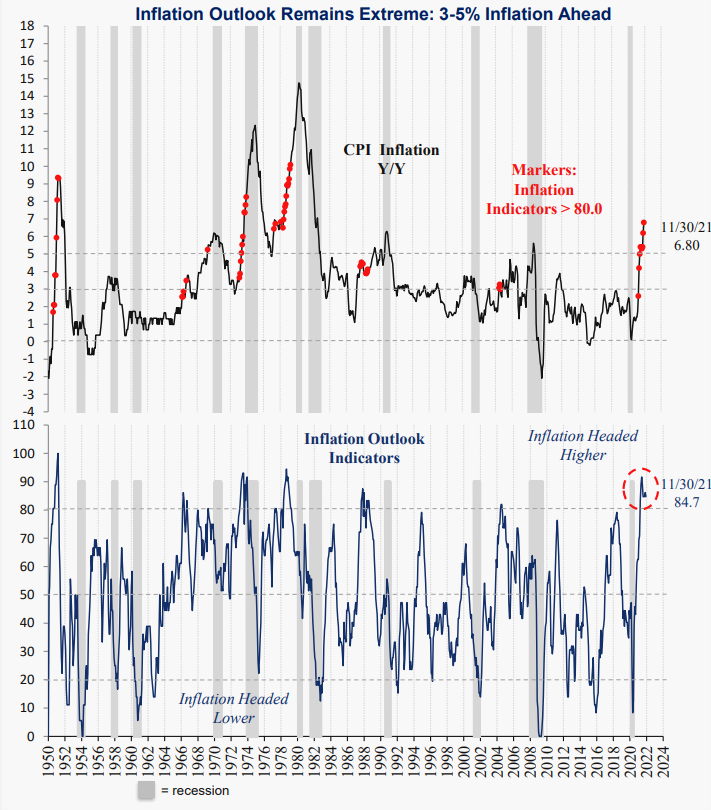

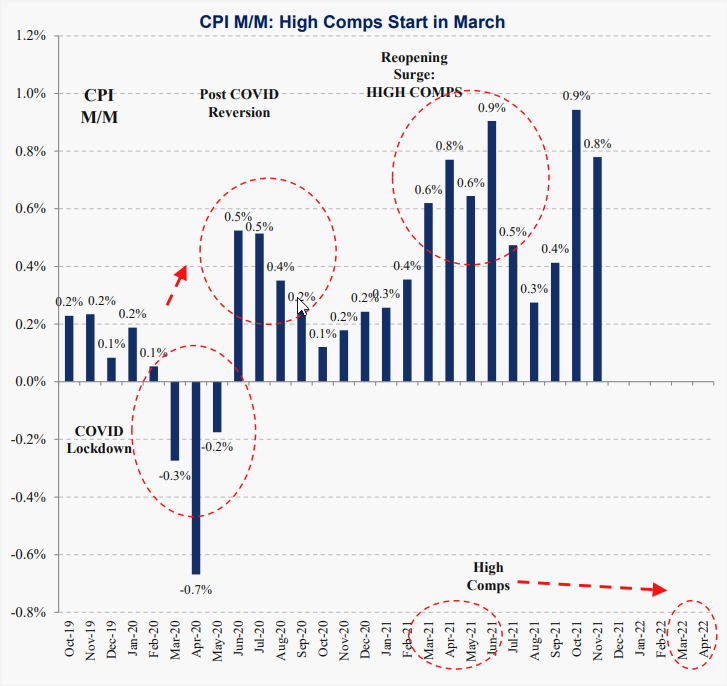

CPI headline inflation reached 6.8% in November, the highest since 1982. It is making headlines on a daily basis and causing political reactions. Our inflation outlook indicators remain high at 84.7, and inflation comps remain low until March. In other words, as we mentioned last month, due to the base effect, it will be difficult for inflation to turn much lower until March when year ago increases were high. The elephant in the room for inflation bulls is why the 10-year yield remains at just 1.5%. Historically the 10-year yield led inflation moves. The ominous fact is aside from the Korean War in 1950, all the prior inflation spikes similar to this year only ended after a recession hit.

However, the more relevant issue is what are the implications for investors today. The short answer is surprisingly positive. Equities are a good hedge against inflation because, for the most part, companies have the ability to raise prices to protect their margins and maintain earnings growth. Obviously on a micro level it is quite complex, since rising input costs like labor could erode earnings instead. A historical test is always helpful to sort theory from reality. Since 1950, the S&P 500 returned a very mixed -0.4% when inflation was over 4% and rising. However, when inflation was over 4% and rising AND monetary policy was loose as it is today, the S&P 500 returned 10.4% annualized. It is only when the Fed tightened policy that equity returns were decidedly negative historically. When the Fed hikes interest rates in earnest, the eventual outcome is usually an equity bear market made deeper due to a recession. For now, however, conditions remain positive.

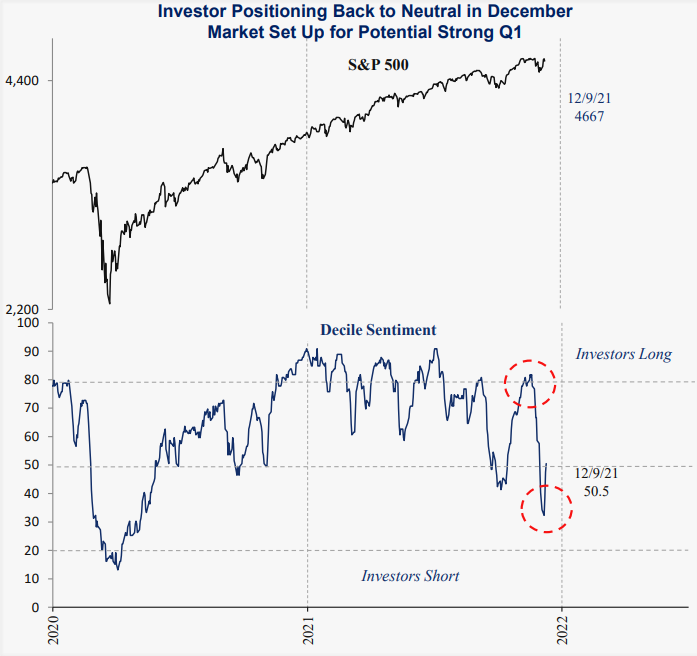

Negative Headlines and Equity Volatility in December: Bullish for Q1

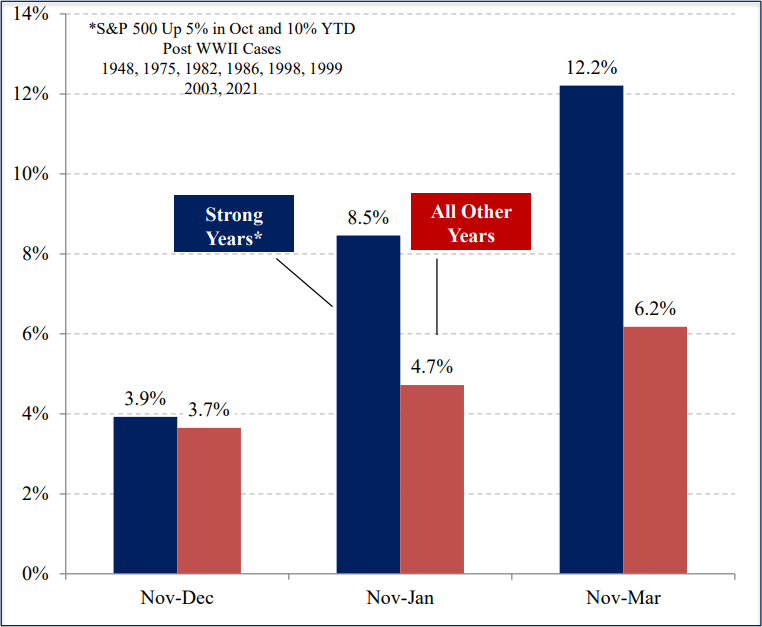

Recent Omicron, inflation and Ukraine headlines combined with the brief 4.1% December decline in the S&P 500 was effective in moving investor positioning from extreme at the November 18th peak back to neutral by mid December. The move effectively removed one of the equity risks going into the New Year. Cash levels and put call ratios rose and surveys of bulls declined across almost all investor groups, generating fuel for the next market advance. In prior years since 1950 the S&P 500 was up strongly in October and YTD, November and December were mixed as the market consolidated gains, then continued higher through the first quarter. Despite such incredible headlines like Omicron, inflation and Ukraine fears, this year is following the pattern. Despite a quick rebound in the S&P 500 to a new high, investor positioning remains neutral, setting the market up for a strong first quarter.

Summary

This month we reviewed economic, monetary and investor positioning indicators and concluded that conditions remain positive for equities at least through the first quarter of 2022. Although there is justified fear of tighter Fed policy ahead, historically the best equity returns were in fact before the initial hike. Inflation and Fed policy are critically important to equity returns, but not always as they are portrayed in the press. We will continue testing conditions as they change. Thank you for your support and please contact your advisor with any questions.

IMPORTANT DISCLOSURES

This review and outlook report (this “Report”) is for informational, illustration and discussion purposes only and is not intended to be, nor should it be construed as, financial, legal, tax or investment advice, of Brenton Point Wealth Advisors LLC or any of its affiliates (“Brenton Point”). This Report does not take into account the investment objectives, financial situation, restrictions, particular needs or financial, legal or tax situation of any particular person and should not be viewed as addressing any recipient’s particular investment needs. Recipients should consider the information contained in this Report as only a single factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of the merits and risks of investments.

This material is based upon information obtained from various sources that Brenton Point believes to be reliable, but Brenton Point makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated and are subject to change without notice.

This Report contains certain forward looking statements opinions, estimates, projections, assessments and other views (collectively “Statements”). These Statements are subject to a number of assumptions, risks and uncertainties which may cause actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by these forward looking statements and projections. Brenton Point makes no representations as to the reasonableness of such assumptions or the likelihood that such assumptions will coincide with actual events and this information should not be relied upon for that purpose. Changes in such assumptions could produce materially different results. Past performance is not a guarantee or indication of future results, and no representation or warranty, express or implied, is made regarding future performance of any financial instrument mentioned in this Report.

Any benchmark shown herein is shown for illustrative purposes only. No index benchmark is available for direct investment. It may not be possible to replicate the returns of any index, as the index may not include any trading commissions and costs or fees, may assume the reinvestment of income, and may have investment objectives, use trading strategies, or have other materials characteristics, such as credit exposure or volatility, that do not make it suitable for a particular person. This is not an offer or solicitation for the purchase or sale of any security, investment, or other product and should not be construed as such. References to specific financial instruments and to certain indices are for illustrative purposes only and provided for the purpose of making general market data available as a point of reference only; they are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities. Investing in securities and other financial products entails certain risks, including the possible loss of the entire principal amount invested, as the value of investment can go down as well as up. You should obtain advice from your tax, financial, legal, and other advisors and only make investment decisions on the basis of your own objectives, experience, and resources.

Brenton Point accepts no liability for any loss (whether direct, indirect or consequential) occasioned to any person acting or refraining from action as a result of any material contained in or derived from this Report, except to the extent (but only to the extent) that such liability may not be waived, modified or limited under applicable law.

This Report may provide addresses of, or contain hyperlinks to, Internet websites. Brenton Point has not reviewed the linked Internet website of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for your convenience and information, and the content of linked third party websites is not in any way incorporated herein. Recipients who choose to access such third-party websites or follow such hyperlinks do so at their own risk.

All marks referenced herein are the property of their respective owners. This Report is licensed for non-commercial use only, and may not be reproduced, distributed, forwarded, posted, published, transmitted, uploaded or otherwise made available to others for commercial purposes, including to individuals within an institution, without written authorization from Brenton Point.

Source of data and performance statistics: Bloomberg L.P. and Factset Research Systems Inc.

©Brenton Point Wealth Advisors LLC 2021

Michael Schaus

Director of Market Research

Michael Schaus is the Director of Market Research for Brenton Point Wealth Advisors and Zweig-DiMenna. Since joining Zweig-DiMenna in 1992, his focus has been on macroeconomic research, the analysis of…

READ MORE

Sign up!

Sign up for our monthly newsletter and get the lastest news and research from our esteemed advisors here at Brenton point. Right into your inbox!